$SMCI: THE PATTERN DOESN'T LIE

Three compliance failures. One co-founder under arrest. And a business that's somehow still growing.

Disclosure: I do not currently own a position in $SMCI.

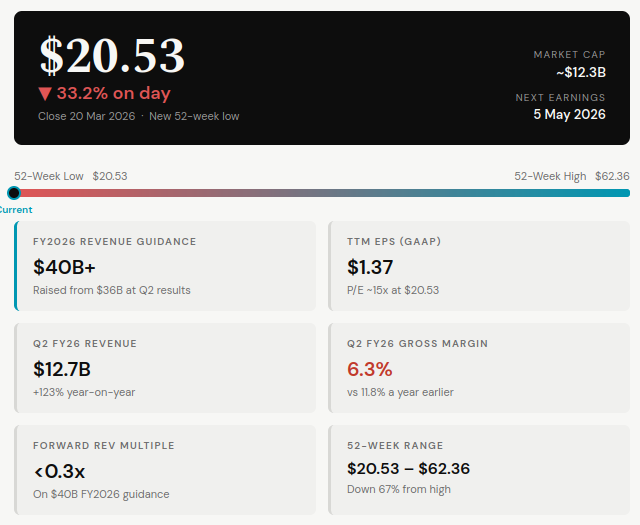

The people who built this company, run it today, and know it better than anyone have made 22 transactions in five years; everyone one of them was a sale. Super Micro Computer closed Friday at $20.53. That is down 33% on the day, the largest single-session decline since October 2018, down 67% from its 52-week high of $62.36, and a new 52-week low.

If you own $SMCI right now or are thinking about owning it, one of two things is true:

1. You bought before today’s stock drop, have potentially held through the compliance crisis of 2024 and the Nasdaq relisting in January 2026, believing the governance issues were now behind the company. You saw revenue triple, the Blackwell cycle arrive and the Q2 FY2026 earnings come in at $12.7 billion and thought the hard part was now over.

2. Or you are looking at this stock today, at ~$20, and you are wondering whether a co-founder under arrest, compressing margins, and a business built almost entirely on Nvidia’s goodwill is actually the entry point of the year, or the kind of value trap that looks cheap for a reason.

Both of those scenarios need the same thing right now: an honest account of what this company actually is, what has happened to it, and what happens next. This is what we’ll be covering today.

The Setup

Super Micro Computer was founded in San Jose in 1993 by Charles Liang, a Taiwanese-American engineer who had previously worked at AMD and Chips & Technologies. Liang’s business idea was that the server market was being under-served by vendors who forced customers into proprietary, inflexible platforms. His answer was a modular, open-standard design philosophy that allowed customers to configure hardware precisely for their workload.

For most of its first two decades, Supermicro was a quietly successful niche operator. Revenue grew steadily, the stock was not exciting, then AI infrastructure spending exploded. Nvidia’s GPU servers became the most demanded hardware on earth, and Supermicro discovered that its liquid cooling technology and assembly speed made it one of the fastest suppliers of GPU-based rack systems in the market. Revenue went from $7.1 billion in 2023 to $14.9 billion in 2024 then to $23.1 billion in 2025. The stock went from under $10 in early 2023 to over $120 at its peak in early 2024.

There is a version of this story where Supermicro is the great infrastructure winner of the AI era, the company that built the physical layer of the data centre faster and cheaper than anyone else. That version is not wrong, the business really has done something remarkable. But this story also includes a company that has now failed its compliance obligations three times in eight years, whose co-founder was arrested on export control charges, and whose governance structure makes it structurally difficult to trust management at face value.

The entire investment question is how do we see this story playing out and if the history of compliance issues continues to repeat itself.

How the Business Works

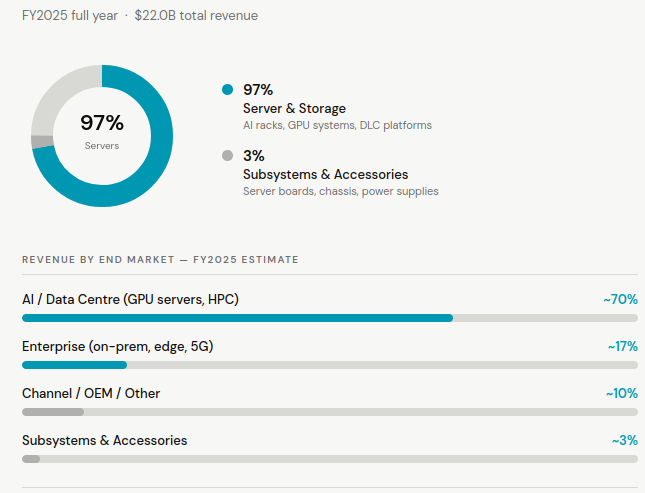

Supermicro is an AI server manufacturer. Its primary business is building the physical infrastructure that houses and connects the graphics processing units that power AI training and inference workloads. The core product is a GPU-based rack system. Supermicro buys primarily Nvidia GPUs, with AMD as a secondary supported platform, integrates them into custom server boards and chassis, applies its liquid cooling technology, and assembles complete rack-scale systems that it ships to data centres. Customers can order standard configurations or work with Supermicro’s engineering team to design custom deployments.

The differentiation has historically rested on three things. First, liquid cooling: Supermicro’s second-generation direct liquid cooling technology, circulates coolant directly to heat-generating components rather than relying on air flow through the rack. Management claims this cuts electricity costs up to 40% and lowers total cost of ownership up to 20% compared with air-cooled deployments. As AI clusters have grown denser and hotter, this capability has moved from a nice-to-have to a core requirement. Second, speed: Supermicro operates with a shorter design-to-shipment cycle than Dell, HPE, or Lenovo. When a new GPU generation arrives, Supermicro typically ships systems weeks before its larger competitors. In a market where hyperscalers are racing to build capacity, that lead time matters. Third, price: Supermicro operates on thin margins and passes those savings to customers, making it competitive on cost.

Numbers Behind the Ramp

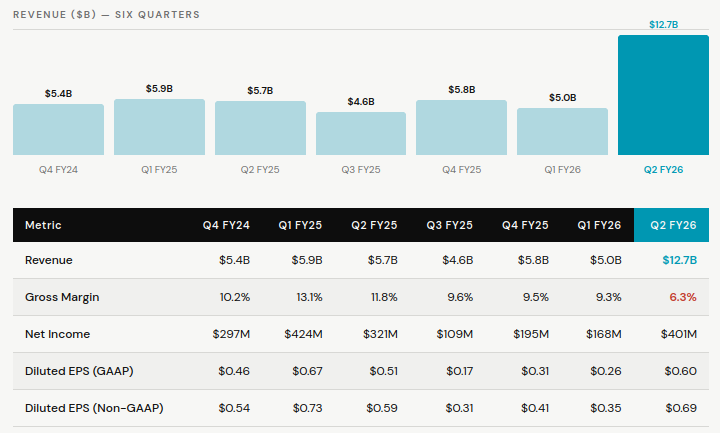

The scale of the AI-driven revenue ramp is genuinely striking. Going from $5.7 billion in Q2 FY2025 to $12.7 billion in Q2 FY2026 in a single year. Full-year FY2026 guidance is $36 to $40 billion, which would represent 64% year-on-year growth on top of an already record year.

The issue with those numbers is margin. Gross margin has compressed from 13.1% in Q1 FY2025 to 6.3% in Q2 FY2026. This reflects a deliberate strategy of pricing aggressively to win large customer contracts, but it also shows that Supermicro’s core activity, buying Nvidia chips and assembling them into racks, is not a high-margin business. The more revenue grows through large hyperscaler deals, the more this margin compresses.

The Nvidia Dependency

Supermicro is almost entirely dependent on Nvidia’s GPU allocation decisions. Supermicro does not design chips, nor does it manufacture the components that determine the performance of its systems. It buys Nvidia’s GPUs, integrates them, and ships them faster and cheaper than its competitors.

That relationship gives Nvidia enormous structural leverage, if Nvidia decided tomorrow to prioritise direct sales or to shift allocations toward Dell, HPE, or its own NVLink-based systems, Supermicro’s revenue would fall sharply. Supermicro’s status as a preferred Nvidia partner is a commercial asset, not a contractual guarantee. The arrest of a co-founder on charges of illegally diverting Nvidia-powered servers to China is not good news for that relationship.

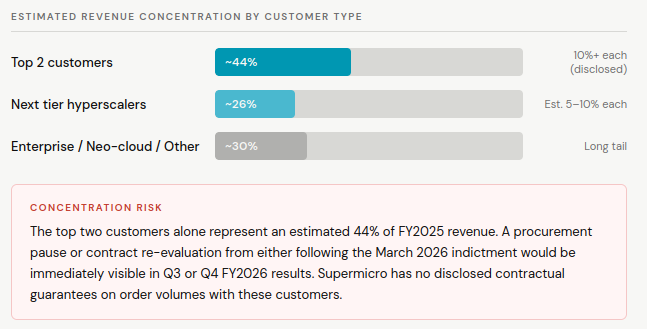

Customer Concentration

Supermicro does not publish a detailed customer list, but its filings have consistently shown that a small number of hyperscalers and large cloud providers account for a disproportionate share of revenue. The shift to mega-deals with these customers is partly what is compressing margins: large buyers have pricing power, and Supermicro has demonstrated willingness to sacrifice margin to retain them. That concentration cuts both ways, it drives the revenue ramp but it also means that the loss of one or two of these customers would be catastrophic.

The Malaysia Campus

Supermicro completed a large-scale manufacturing facility in Malaysia in late 2025. The strategic rationale makes sense: lower-cost assembly, reduced US tariff exposure for export markets, and geographic diversification away from the San Jose-and-Taiwan-centric operations. The facility is also where some of the questions around export control compliance have become more pressing, servers assembled in Malaysia and shipped onward are exactly the kind of configuration that regulators scrutinise when investigating potential exports to restricted end-users.

The Pattern: Three Failures in Eight Years

The single most important thing both existing and prospective investor needs to understand about Supermicro is nothing to do with AI. It is the fact that this company has now experienced three distinct compliance crises in eight years, each one involving the same core governance weaknesses.

First Compliance Failure: 2017 to 2020

In 2017, Supermicro missed an annual SEC filing deadline and received an extension. It then missed that extension and was formally delisted from the Nasdaq in August 2018 after an SEC probe into revenue recognition practices. This delisting forced it to trade on the OTC market. It took until 2020 to settle with the SEC, restate its financials, and regain its Nasdaq listing. The settlement involved no admission of wrongdoing, a $17.5 million penalty, and a commitment to implement enhanced internal controls.

The lesson the company appeared to take from that experience was that it could survive a compliance crisis and emerge with the business intact. That lesson was then reinforced when the stock recovered and AI demand arrived in 2023.

Second Compliance Failure: August 2024 to January 2026

In August 2024, short-seller Hindenburg Research published a report alleging accounting manipulation, undisclosed related-party transactions, and export control violations. The company did not file its annual 10-K on time, Nasdaq then issued a non-compliance notice on 17 September 2024.

On 24th October 2024, Ernst & Young resigned as auditor. This was not a routine auditor change, EY had been present for only eighteen months. In its resignation letter, EY stated it was unwilling to be associated with financial statements prepared by management and that it could no longer rely on management’s representations to the audit committee. Auditors do not just resign mid-engagement from public companies unless they have concluded the situation is serious. EY’s departure was one of the clearest governance red flags a public company can produce.

The Department of Justice launched an investigation, a special committee of the board was convened, then BDO USA was hired as replacement auditor. The special committee’s report in late 2024 found no evidence of misconduct, a conclusion that allowed the company to file its delayed reports and regain Nasdaq compliance on 27th January 2026.

Then just fifty-three days later, the company’s co-founder was arrested.

Third Compliance Failure: March 2026

On 19th March 2026, the United States Attorney’s Office for the Southern District of New York unsealed an indictment charging three individuals associated with Supermicro: co-founder and Senior Vice President of Business Development; Yih-Shyan Wally Liaw, a sales manager in Taiwan; Ruei-Tsang Steven Chang (now a fugitive) and a contractor; Ting-Wei Willy Sun.

The charges: one count of conspiring to violate the Export Controls Reform Act, one count of conspiring to smuggle goods from the United States, and one count of conspiracy. Prosecutors allege that between 2024 and 2025, the group used fabricated end-user documentation and a pass-through intermediary to divert approximately $510 million worth of Nvidia-powered servers to Chinese end-users, in violation of US export controls. Liaw and Sun were arrested. Chang remains at large.

Supermicro has since issued a statement confirming it was not named as a defendant, placed its two employees on administrative leave, and terminated its relationship with the contractor. The company stated the conduct was contrary to its policies and compliance controls. On 20th March 2026, the company announced that Liaw had resigned from the board with immediate effect, reducing the board to eight directors. The same announcement named DeAnna Luna, an Intel and Teledyne veteran who had joined Supermicro in 2024 as VP of Global Trade and Sanctions Compliance, as acting Chief Compliance Officer. The stock closed down 33% on the day, erasing over $6 billion in market value in a single session.

The indictment period across 2024 to 2025 overlaps directly with the second compliance issue, meaning this was going on whilst the special committee was investigating governance failures and whilst Ernst & Young was raising concerns about management’s representations. Whether those two things are connected is something prosecutors will determine, but the timeline is not a coincidence. The operational detail in the indictment is worth noting. According to prosecutors, the scheme involved a warehouse in Southeast Asia stocked with dummy server shells. When Supermicro compliance auditors arrived to verify end-user locations, they photographed rows of servers with visible serial numbers. What they were photographing were empty chassis. The real servers, loaded with Nvidia GPUs, had already been forwarded to Chinese customers. Serial number stickers had allegedly been transferred from the real hardware to the dummy shells. A compliance auditor was allegedly bribed to file a clean report. This was not a simple paperwork error. It was an active, multi-step deception of the company’s own compliance function.

Management and Insider Activity

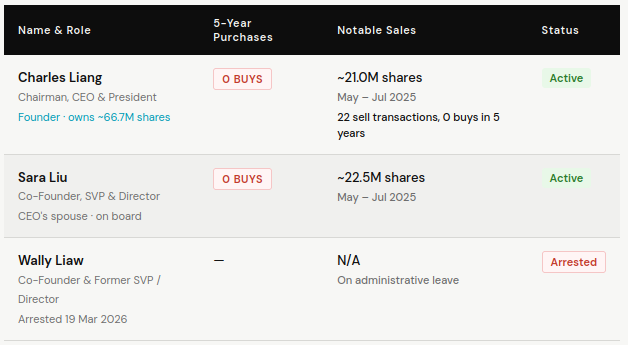

Charles Liang: Chairman, CEO, and President

Charles Liang founded Supermicro in 1993 and has run it since. He takes a $1 annual salary with no cash bonus and no restricted stock units. His compensation is structured entirely through performance options, with vesting tied to both stock price milestones and revenue targets, with sale restrictions on his 2023 option grant until 14 November 2026. The framing is that Liang’s incentives are fully aligned with shareholders.

The reality of his trading record complicates that framing, according to SEC filings, Liang has made 22 transactions in Supermicro over the past five years. The number of purchases in that period is zero. Between May and July 2025, when the stock rallied on Blackwell cycle momentum and the company was still in the middle of its compliance recovery, Liang sold approximately 20.98 million shares.

The CEO’s sale restriction until November 2026 on his 2023 options is worth touching on. Once that restriction lifts, Liang will hold a further 10 million fully vested shares plus potential additional tranches. The supply overhang from those positions will likely create selling pressure in the second half of 2026, independent of any compliance related news.

Sara Liu: Co-founder, SVP, and Director

Chiu-Chu Sara Liu is Charles Liang’s wife. She is also a co-founder of the company, its Senior Vice President, and a member of its board of directors. She sold 22.5 million shares in the May to July 2025 rally like her husband.

The governance concern here is not subtle, having the CEO’s spouse as a board director, in a company where the CEO has historically resisted external oversight and where there have been three compliance crises in eight years, makes board independence difficult to assert. This is a governance structure that was raised in the Hindenburg report and is visible in any reading of the company’s proxy filings.

Wally Liaw: Co-founder, SVP Business Development, and Former Board Member (Arrested)

Yih-Shyan Wally Liaw was a founding member of Supermicro, served as Senior Vice President of Business Development, and sat on the board of directors. He is now under federal indictment on export control charges, has been placed on administrative leave, and resigned from the board with immediate effect on 20th March 2026. He is a US citizen. He was arrested on 19th March 2026 and released on bail.

A co-founder and board director being criminally charged is not an everyday event for a company of this size, especially considering he sat on the board reviewing the very compliance controls the company was publicly committing to strengthen.

The Insider Activity Summary

There has not been a single insider purchase of Supermicro stock by a named executive in five years. That includes the periods of maximum AI optimism and the periods following the compliance crisis resolution. The people who know this company best have been consistent sellers throughout.

The Partner Question

The arrest of a co-founder on charges of illegally diverting Nvidia-powered servers to China creates a specific risk that goes beyond Supermicro’s own compliance exposure. It potentially causes problems with every significant relationship the company has.

Nvidia

Nvidia’s entire export control programme is built around the premise that it sells to authorised channel partners who enforce end-user restrictions. Supermicro is one of the most significant of those partners globally, if a co-founder and board member was allegedly diverting Nvidia-powered servers to Chinese end-users for two years, the question for Nvidia is pretty straightforward: what did it know, when did it know it, and what does it need to do now to demonstrate to the Department of Commerce that its channel controls are adequate?

Nvidia is already navigating extreme regulatory sensitivity around China exports. When the indictment broke, Nvidia issued a statement stating that strict compliance is a top priority and that unlawfully diverted systems receive no service or support from Nvidia. The statement was carefully worded, distancing Nvidia from the conduct without addressing its commercial relationship with Supermicro directly. Supermicro accounts for approximately 9% of Nvidia’s revenue according to Bloomberg, that is too large a share to sever overnight, but the statement signals that Nvidia will not be providing any cover for its channel partner.

The relationship is not going to evaporate overnight, Supermicro represents too large a share of Nvidia GPU deployment to simply be cut off without disrupting Nvidia’s own revenue. But the possibility that Nvidia redirects future allocations towards other partners with cleaner governance structures, such as Dell.

Has Anyone Left Before?

During the 2024 compliance crisis, the question of customer and partner defection was raised repeatedly. The answer in 2024 was largely no, as the demand for GPU servers was so extreme that customers could not afford to wait for alternative suppliers to spin up capacity. Supermicro was shipping product that Dell and HPE simply could not match at the same speed and price point.

The situation today is different in one important respect. Dell’s AI server revenue in Q4 FY2026 was $9.0 billion, up 342% year on year. Dell has now demonstrated it can ship at scale, the capacity constraint that protected Supermicro during the 2024 crisis no longer applies to the same extent and if a hyperscaler that wants to reduce its Supermicro exposure it now has a credible alternative.

Singapore’s investigation in early 2025 into servers shipped by both Dell and Supermicro to Malaysia, suspected of containing chips subsequently forwarded to China, is an important distinction. Dell was named as a deceived supplier, not a willing participant. Singapore’s authorities concluded that the fraud was carried out by intermediaries who misled Dell about the true end-users. Dell responded immediately with a public statement confirming it maintains a strict trade compliance programme, screens all orders through an internal due diligence system, and terminates relationships with non-compliant customers. When Nvidia subsequently instructed its major channel partners to conduct spot checks on Southeast Asian customers, Dell acted on that instruction, Supermicro on the other-hand did not respond to press queries at the time. The contrast in how the two companies handled the same situation is part of why the market is treating Dell as the governance-clean alternative today.

Will Partners Stay?

The honest answer is that no one knows yet. The critical variable is whether federal prosecutors expand the investigation to the corporate entity itself, the current indictment names three individuals and does not charge Supermicro as a company. If that changes, a company under criminal indictment faces a different set of procurement restrictions, particularly from government-adjacent hyperscalers and defence contractors.

Even absent corporate charges, Supermicro faces a procurement review process at every major customer, contract renewals will now include compliance certification requirements that were not previously standard. Some customers will quietly reduce concentration, some won’t. The revenue impact will not show up in Q3 FY2026 guidance but it may show up in Q4 and beyond.

What the Legal Timeline Actually Looks Like

Export control cases move slowly. The first compliance crisis took from 2017 to 2020 to resolve. The second took from August 2024 to January 2026. The third is beginning now, and it is criminal rather than regulatory.

Criminal proceedings in federal court, particularly complex financial and export control cases, typically take eighteen months to three years from indictment to resolution. During that period, the case will generate regular news events: bail hearings, pre-trial motions, document demands, witness interviews, with each event being a potential stock catalyst.

The current indictment is against three people, if prosecutors develop evidence that the conduct was known to, directed by, or systematically enabled by Supermicro as a corporate entity, a separate corporate indictment becomes possible. The consequence of this would be far more severe triggering mandatory contract review clauses at government customers, potentially restrict the company’s ability to export, and could result in denial of export privileges, which would effectively end Supermicro’s ability to sell AI servers containing any controlled US technology outside the United States, including both Nvidia and AMD GPUs.

The probability of a corporate indictment isn’t high, but it’s also not zero. The conduct alleged was carried out by a board member using company employees and infrastructure over multiple years. Prosecutors will be looking at what management knew and when, with the special committee report from late 2024 that found no evidence of misconduct being re-reviewed.

The Numbers

The revenue jump from Q1 to Q2 FY2026, $5.0 billion to $12.7 billion in a single quarter, reflects the Blackwell cycle arriving. Nvidia’s B200 and GB200 systems reached commercial scale in Q4 2025, and Supermicro’s speed-to-market advantage translated directly into share capture during the initial rollout.

The margin story is harder to explain away, at 6.3% gross margin, Supermicro is generating revenue at a scale that most hardware companies would celebrate while earning margins that most software companies would be looking to improve. The company’s argument is that margins will recover as the Blackwell ramp matures and service revenue grows. The counter-argument is that mega-deal pricing pressure is structural, not cyclical, and that any margin recovery will be competed away by Dell and HPE as they close the capability gap. The new compliance issues also further complicate this picture, with existing clients potentially looking to reduce exposure may add further pressure on margins at contract renewal.

FY2026 Guidance and Valuation

At roughly 15x trailing earnings and a forward revenue multiple of under 0.3x on $40 billion guidance, Supermicro does not look expensive on pure financial metrics. The governance discount is baked into those numbers. The key question is whether that discount appropriately prices the legal risk described earlier, or whether the market is still underestimating the corporate indictment risk and the possibility of meaningful partner defection.

The Bull Case

The bull case requires believing four things simultaneously:

1. The criminal case stays contained to the three named individuals and doesn’t expand to Supermicro itself.

2. Nvidia doesn’t materially reduce Supermicro’s GPU allocation and the commercial partnership survives.

3. Hyperscaler customers don’t significantly reduce their exposure to Supermicro and the Q3 and Q4 orders remain close to guidance.

4. Gross margins begin recovering in the second half of 2026 as the service revenue mix improves and the Blackwell roll-out matures.

If all four of these play out, you have a company trading at under 0.3x forward revenue, at roughly 15x trailing earnings, generating $12.7 billion per quarter in revenue, with a multi-year AI infrastructure tailwind and a liquid cooling technology advantage.

The issue with the bull case is that it requires trusting a management team whose governance track record is objectively poor, in a situation where the legal outcome is entirely outside management’s control.

The Bear Case

The bear case does not require a full corporate indictment, it only requires that one or two of the bull case conditions fail:

1. If Nvidia reduces allocations by just 20% in favor of other suppliers such as Dell, Supermicro’s revenue trajectory breaks.

2. If just one or two hyperscaler customers reduce concentration, the revenue and margin compression begins to snowball.

3. If the legal proceedings extend over years and generate adverse news events, the governance discount deepens and the cost of capital rises.

4. If margins do not recover and the company is generating $40 billion in revenue at sub-7% gross margins, the earnings power does not justify the current multiple.

The most dangerous version of the bear case is the corporate indictment scenario, a company under criminal indictment for export control violations cannot export. Given Supermicro’s entire business model is exporting Nvidia-powered AI servers, then it no longer has a viable business.

Valuation and Scenario Analysis

The stock closed Friday at $20.53, the base case is not a recovery story, it’s about stabilisation. The downside cases are not abstract tail risks, they are plausible outcomes that the market has not yet fully priced.

Final Thoughts

Supermicro is an impressive operational business that has built a meaningful position in AI infrastructure through real engineering capability and real commercial execution. The liquid cooling technology is differentiated, its speed-to-market advantage is real and proven. The revenue trajectory, if it holds, is extraordinary. But the margin story sits uneasily alongside all of it, gross margin has collapsed from 13.1% to 6.3% in four quarters. The company is generating $12.7 billion in quarterly revenue while earning margins that do not reflect a business with meaningful competitive moat.

However the company has now failed its compliance obligations three times in eight years. The first time cost it its Nasdaq listing for two years. The second time cost it its auditor, triggered a DOJ investigation, and nearly cost it its listing again. Now the third time involves a co-founder under criminal arrest on charges that go to the heart of the company’s relationship with its most important commercial partner.

The market has repriced Supermicro sharply on the arrest news, whether it has repriced it enough depends on a variable that no financial model can resolve: will federal prosecutors conclude that the conduct of three individuals was their own initiative, or was it was something the company enabled and protected.

For existing holders: the fundamental question is whether you believe the legal case stays contained and the Nvidia relationship survives. If yes, the current price offers a reasonable entry to add. If there is any doubt on either count, this is not the moment to increase exposure, the legal timeline will provide regular inflection points over the next eighteen months.

For prospective buyers: you are being asked to buy a company at a governance discount, in a legal situation with significant tail risk, on the basis that the business fundamentals are strong enough to compensate. That might be true, but the insider trading record, the board composition, and the compliance history all suggest that the people who know this company best have been consistent sellers.

The next meaningful data point will be the Q3 FY2026 earnings on 5th May 2026. Watch the order guidance, any commentary on customer concentration, and above all, any further statements from Nvidia on its channel partner relationship with Supermicro.

I’m just a guy with a keyboard, some spreadsheets and too many tabs open. This is not investment advice, make your own mistakes.