$ORCL: The $523 Billion Question

The AI infrastructure bet that broke the balance sheet, and might still be right

Disclosure: I don’t currently own a position in $ORCL.

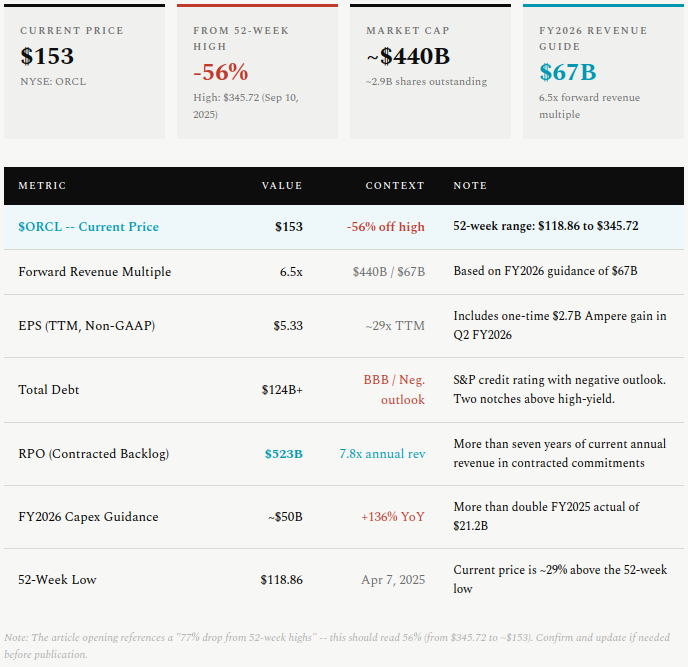

A stock down 56% from its 52-week highs. Thousands of layoffs announced this week. Earnings in two days.

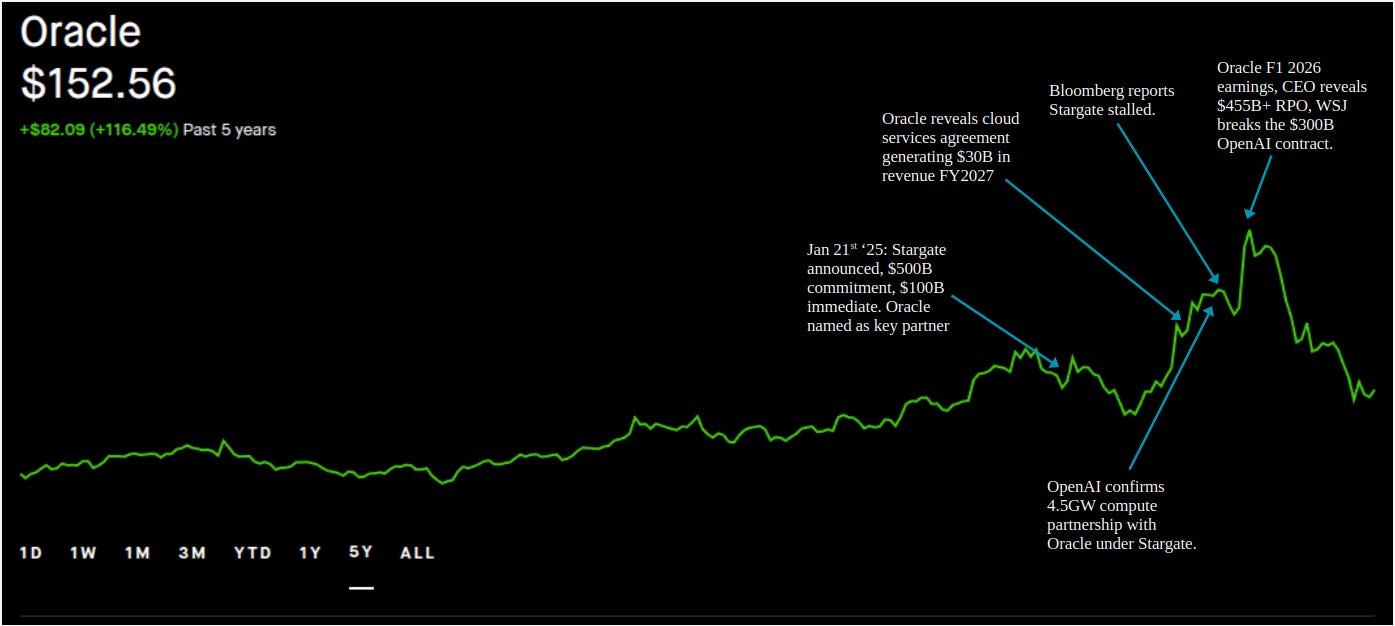

If you own $ORCL right now, you’re probably somewhere between confused and furious. The stock peaked at $345.72 in September ‘25 and it’s now sitting around $153. That kind of drop usually means one of two things: the market has figured out that the business is broken, or the market has completely lost the plot on a company making the most important infrastructure bet in enterprise tech history. Right now, the business and the stock are telling completely different stories.

Here’s what makes this genuinely hard: the business hasn’t fallen 56%. In Q2 FY2026, cloud revenue grew 34% and Oracle Cloud Infrastructure grew 68%. The company has $523 billion in contracted future revenue. It just completed a $25 billion bond sale that attracted $129 billion in orders. Yet the stock is at its lowest level since early 2025.

And this week, Bloomberg reported Oracle is planning to cut between 20,000 and 30,000 employees to free up cash for its AI data centre buildout.

So the question I want to answer is this: is Oracle a company that’s over-extended itself beyond recovery, or is this the most interesting entry point in enterprise tech this year?

Q3 FY2026 earnings land on Tuesday, March 10th. Let’s get into it.

The Setup

Oracle’s story is the story of a company that was supposed to be the slowest boat in the cloud race, and then suddenly wasn’t.

For most of the last decade, Oracle’s cloud narrative was a story of missed opportunity. While Amazon, Microsoft and Google were building hyperscale infrastructure through the 2010s, Oracle was defending its legacy database business. By the early 2020s, the market’s view of Oracle was largely settled: great database, mediocre cloud, slow-moving management. A business in gradual decline.

What changed the story was the architecture Oracle had quietly built. Oracle Cloud Infrastructure was designed from the start around ultra-high speed networking, originally to support database workloads. When AI labs started looking for compute at scale, they found that the hyperscalers were expensive and capacity-constrained. Oracle’s networking was faster and cheaper for distributed AI training than anything AWS or Azure could offer at equivalent scale.

OpenAI noticed. On September 10th ‘25 they reported a $300 billion, five-year contract that rewrote the Oracle narrative overnight. The stock surged ~42% overnight to $345, as investors repriced Oracle from legacy software vendor to AI infrastructure play.

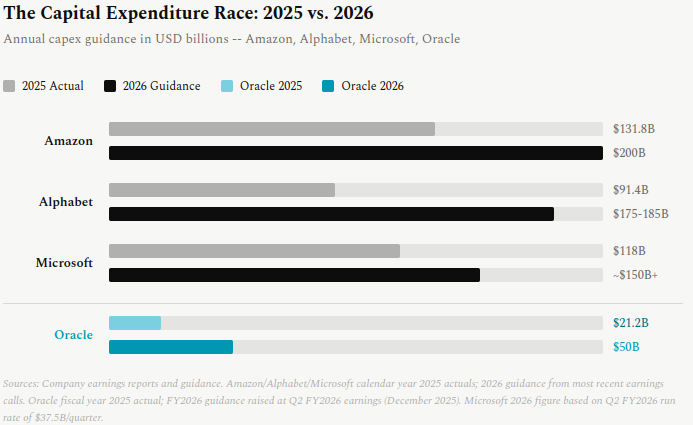

Then reality kicked in. The spending required to fulfil those commitments is staggering: Oracle is targeting approximately $50 billion in capital expenditure in a single fiscal year, more than double what it spent in FY2025. Here’s the timeline of what happened next.

How the Business Works

Oracle runs three business segments, but for this thesis we will focus on cloud, where the major growth and risk are: the infrastructure business growing at 68%, and the legacy software business quietly funding everything.

Oracle Cloud Infrastructure (OCI):

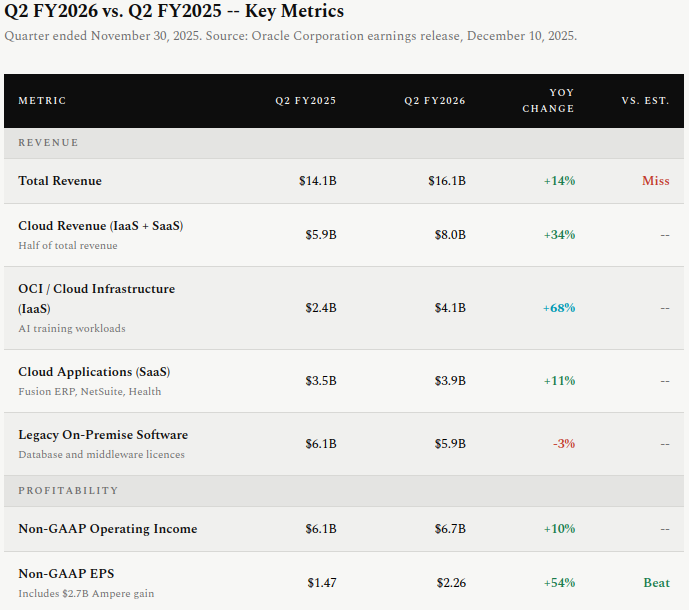

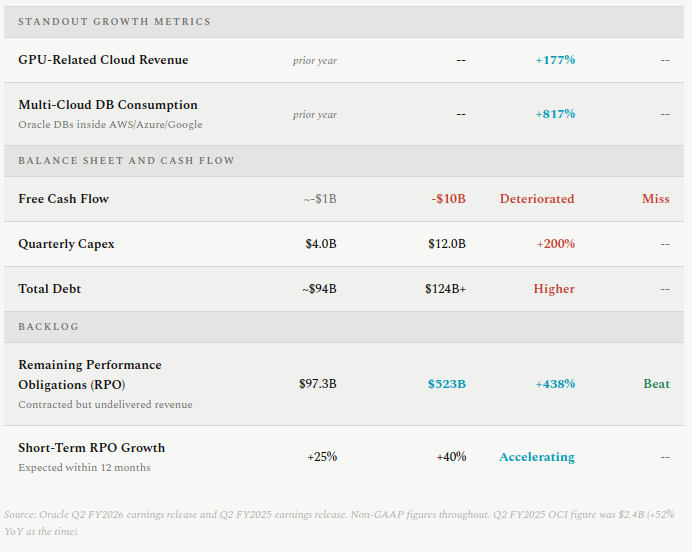

This is the AI infrastructure engine. OCI provides the compute, storage and networking that AI labs use to train and run models. In Q2 FY2026 it generated $4.1 billion in revenue, up 68% year-over-year. GPU-related cloud revenue grew 177% in the same period. Multi-cloud database consumption, where customers run Oracle databases inside AWS, Azure or Google Cloud, grew 817%.

OCI is where the Stargate contracts live, where OpenAI’s training workloads run, and where the bull thesis either plays out or doesn’t.

Cloud Applications (SaaS):

Oracle’s software-as-a-service business: Fusion Cloud ERP, HCM, NetSuite, and Oracle Health. It generated $3.9 billion in Q2, up 11% year-over-year. Fusion ERP grew 18%, NetSuite grew 13%. Steady, highly profitable, and provides the recurring cash flow that partially offsets the infrastructure spending.

Legacy On-Premise Software

The original Oracle business: database and middleware licences. Still generating $5.9 billion in quarterly revenue but declining 3% year-over-year as customers migrate to cloud. Highly profitable. Think of this as the engine that’s been paying for the transformation.

The Stargate Bet

Stargate is a joint venture between Oracle, OpenAI and SoftBank, announced at the White House January 21st ‘25. The plan: invest up to $500 billion in AI infrastructure in the United States by 2029. Oracle is the infrastructure provider.

The anchor contract is a reported $300 billion, five-year deal with OpenAI. To fulfil it, Oracle is building data centres at gigawatt scale. The flagship campus in Abilene, Texas is operational. Oracle and OpenAI have committed to an additional 4.5 gigawatts of capacity across five additional sites. At Q2 FY2026, Oracle had over 211 live and planned cloud regions worldwide, more than any competitor.

The economics Oracle is targeting: $135 billion in infrastructure spend generates $300 billion in revenue, with roughly 40% gross margins once capacity is built and utilized. That’s the maths behind the bet. The problem is you have to spend the $135 billion before you collect the $300 billion.

The Big Picture

The Market Opportunity

The AI infrastructure market is not a niche. According to Goldman Sachs research, hyperscalers and AI companies are projected to spend over $1.155 trillion on data centre infrastructure from 2025 to 2027 alone, with that figure expected to grow significantly through 2030. Oracle isn’t trying to win all of that. It’s trying to win a specific slice: the compute-intensive, latency-sensitive, large-scale AI training workloads where OCI’s networking architecture gives it a genuine edge.

The database market provides a second growth vector. Oracle’s technology runs across the majority of Fortune 500 enterprises. As those companies build AI applications, they need to run models against their existing data. Most of that data lives in Oracle databases. The multi-cloud strategy turns that installed base into a revenue stream that grows regardless of where AI workloads are hosted.

The sovereign cloud opportunity is a third vector that gets less attention. Governments won’t store sensitive national data in standard hyperscale environments. The reason AWS, Azure and Google Cloud are structurally constrained here isn’t just political, it’s legal. Under the US CLOUD Act, any American-headquartered cloud provider can be compelled to hand over customer data stored anywhere in the world if the US government requests it. For a foreign ministry, intelligence agency or defence department, that’s an unacceptable risk regardless of where the servers physically sit. Oracle faces the same legal jurisdiction, but its sovereign cloud model is built differently. Rather than simply offering data residency guarantees, Oracle deploys physically isolated, air-gapped environments operated entirely by local nationals in the customer’s own country, under local law, with Oracle personnel having no operational access. The customer’s own government runs it. AWS and Azure have launched their own sovereign cloud products, but both retain operational control, which means they remain subject to US law in a way that undermines the core promise. Oracle’s model doesn’t just keep data local. It keeps Oracle out. These contracts are long-duration, non-cyclical, and largely immune to the budget pressures that affect commercial cloud spending.

The Macro Backdrop

The AI capex supercycle is the most powerful structural tailwind in enterprise tech right now. Every major technology company, and an increasing number of governments, are making multi-year commitments to AI infrastructure. The companies best positioned to absorb that spending are those with the physical infrastructure, the existing customer relationships, and the technical architecture to actually deliver it at scale.

The risk to that backdrop is a slowdown in AI investment if model capabilities plateau or the economics of AI deployment disappoint. If the AI applications being built on Oracle’s infrastructure don’t generate returns for the companies paying for them, the investment cycle slows. That’s not Oracle’s specific risk, it’s a market-wide risk, but Oracle is more exposed to it than most because of the scale of its commitment.

Management

Larry Ellison: Chairman and CTO

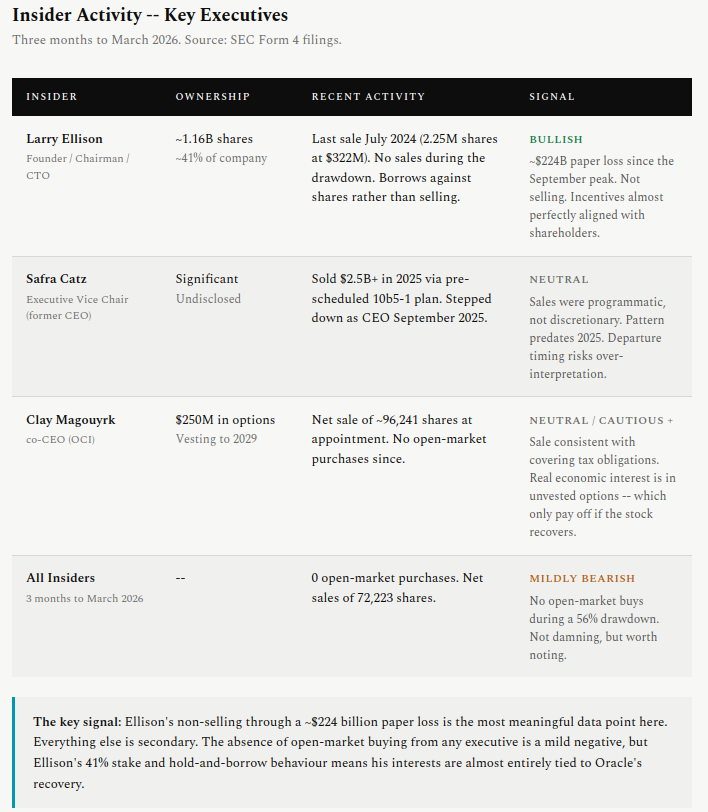

Ellison founded Oracle in 1977 and has been its dominant force for nearly five decades. He stepped back from the CEO role in 2014 but retained the Chairman and CTO titles, and in practice he has never stepped back from anything. The Stargate bet, the OpenAI relationship, the decision to spend $50 billion in a single fiscal year on infrastructure: these are Ellison’s calls. He runs Oracle’s technology strategy and holds around 41% of the company’s outstanding shares.

That ownership figure is the thing to understand about Ellison. He owns approximately 1.16 billion shares. At the September 2025 peak he was briefly the world’s wealthiest person, with a net worth around $400 billion. He has since lost roughly $224 billion of that on paper as the stock has fallen. He is, by a considerable margin, the most exposed person to Oracle’s success or failure. His incentives are aligned with shareholders in a way that most executives’ aren’t.

His track record with bold technology bets is worth noting. OCI was dismissed as irrelevant for years. It is now growing at 68% and hosting OpenAI’s training workloads. The pattern suggests someone who is willing to be wrong for a long time in pursuit of being eventually right.

Co-CEOs: Clay Magouyrk and Mike Sicilia

In September 2025, at the peak of Oracle’s stock price, Safra Catz stepped down as CEO after eleven years. She was replaced by two insiders appointed as co-CEOs simultaneously.

Clay Magouyrk, 39, is the OCI story in human form. He joined from Amazon Web Services in 2014, was a founding member of Oracle’s cloud engineering team, and has led OCI through its transformation from irrelevant to essential. He was handed $250 million in stock options when he was appointed CEO, with 80% vesting over four years and 20% tied to specific revenue performance metrics.

Mike Sicilia, 54, joined Oracle through the Primavera acquisition in 2008 and built Oracle’s industry applications business. His expertise is in vertical AI: deploying AI agents into specific regulated industries like healthcare, banking and hospitality where Oracle’s established relationships give it a structural advantage. He received $100 million in options on the same structure.

Catz remains on the board as Executive Vice Chair. Having the person who ran the company for eleven years still in the building, and still close to Ellison, provides continuity. The co-CEO model has a mixed track record at large companies. The risk is clear enough. But both appointments are deeply operational insiders who have spent years inside the specific businesses they now run. This isn’t a transition to outsiders.

Insider Activity

The insider picture at Oracle tells a nuanced story. The table below covers the key players.

The Numbers

Q2 FY2026 (ended November 30, 2025) is the last full quarter we have, the numbers are a mixed picture.

The market focused on the negatives when these came out on December 10th, and had reasons to. Revenue missed consensus by roughly $100 million, which doesn’t sound like much on a $16 billion quarter but was the eighth miss in ten quarters. Capex guidance was raised by $15 billion. Free cash flow was twice as negative as expected.

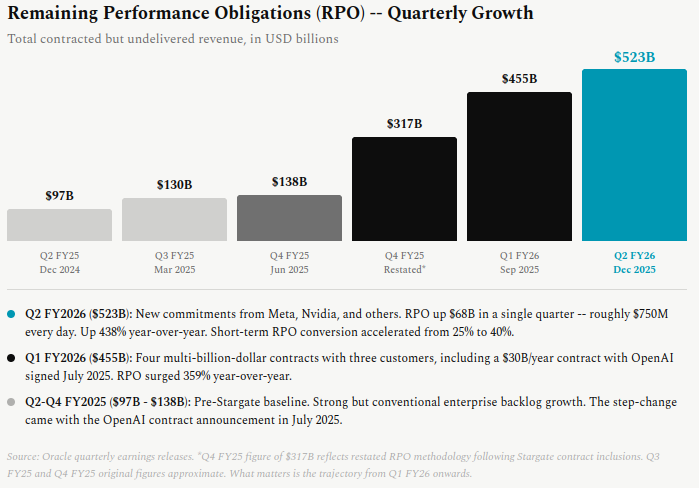

The number that matters most for the investment thesis is the Remaining Performance Obligations (RPO); the total value of contracts signed but not yet delivered, essentially Oracle’s order backlog.

$523 billion in RPO means Oracle has more than seven years of current annual revenue in contracted commitments. That figure went up by $68 billion in a single quarter, roughly $750 million every day, driven by new commitments from Meta, NVIDIA and others. Short-term RPO, the portion expected to convert within twelve months, grew 40% year-over-year, accelerating from 25% the prior quarter.

That acceleration in short-term RPO is the most important data point in the whole story. It means the backlog isn’t just growing. It’s starting to convert faster.

What to Watch on Tuesday

Analyst consensus for Q3 FY2026 sits at revenue of $16.9 billion (19% growth) and non-GAAP EPS of $1.71. Oracle’s own guidance was cloud revenue growth of 40-44% and total revenue growth of 19-21%, with non-GAAP EPS of $1.70-$1.74. The bar is clearly set.

1. Does OCI acceleration continue?

68% in Q2 was strong. The bull thesis requires that trajectory to hold or improve as new capacity comes online. Anything above 70% would be taken positively. A deceleration would raise immediate questions about whether the most important growth engine is losing momentum.

2. What happens to RPO?

$523 billion set a high watermark. Another meaningful sequential jump, particularly in short-term RPO, validates that the backlog is converting and that new contracts are still being signed at pace. A slowdown here would raise questions about whether the bookings cycle has peaked.

3. What does management say about the layoffs?

The reported 20,000-30,000 job cuts were not in the script a week ago. Investors will want to understand whether this is proactive cost management or a more urgent cash crunch driving the decision.

4. Does capex guidance move again?

Oracle raised full-year capex from $21 billion in FY2025 to approximately $50 billion for FY2026. Any further increase would amplify balance sheet concerns. Any signal that the peak is visible from here would be meaningfully positive.

5. What’s the Blue Owl update?

The FT reported that Blue Owl Capital pulled from funding a $10 billion Oracle data centre project. Oracle subsequently completed a $25 billion bond sale, suggesting it found alternative capital. Understanding who is now funding the buildout, and at what cost, matters significantly for the debt picture.

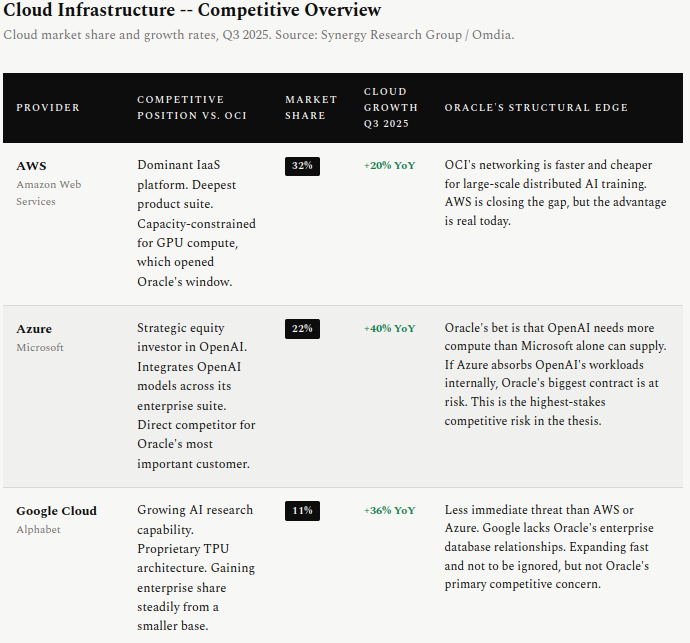

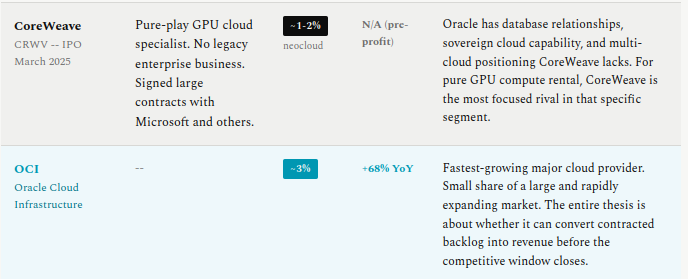

The Competitive Landscape

Oracle isn’t competing against AWS, Azure and Google Cloud on their own terms. It’s trying to win a specific corner of the market where those platforms have structural disadvantages, while defending its existing enterprise database business against the same giants.

The honest summary: Oracle has a genuine and differentiated position for large-scale AI training workloads. That position is real now, but it is not permanent. Every hyperscaler is expanding capacity aggressively. The window of Oracle’s competitive advantage on pure infrastructure is measured in two to three years, not ten.

The Depreciation Problem

This is the accounting issue that won’t go away, and it matters more for Oracle than almost any other company in the AI trade. In November 2025, Michael Burry (the investor from The Big Short) posted a series of claims arguing that hyperscalers including Oracle, Meta, Microsoft, Google and Amazon are overstating their earnings by stretching the “useful life” they assign to their AI hardware. He estimated this could overstate industry profits by more than 20%, with roughly $176 billion of depreciation understated across the sector between 2026 and 2028.

The accounting, simplified.

When a company spends $1 billion on servers and GPUs, that $1 billion doesn’t hit the income statement on day one. Instead, accounting rules require the company to spread that cost over the expected useful life of the equipment. This spreading is called depreciation.

So if Oracle buys $1 billion worth of Nvidia GPUs and decides those chips will last 3 years, it books around $333 million in depreciation expense each year. If it decides they’ll last 6 years, it books $167 million a year instead. The cash going out the door is exactly the same. The hardware cost is exactly the same. But the hit to reported earnings is half as large under the longer assumption.

This is entirely legal. Under GAAP, companies are required to use their best estimate of an asset’s useful life, and that estimate is management’s call. Auditors review it, but it’s inherently subjective. The problem is that “subjective” creates an obvious incentive when you’re spending $50 billion a year on hardware and the choice between a 3-year and 6-year depreciation schedule is worth billions in reported profit.

What Oracle actually does

Oracle has extended its server and networking equipment depreciation schedule from 4 years to 5 years, and then to 6 years, over the past several years; in lockstep with the wider industry. According to SEC filings and analyst research, Oracle currently uses a 6-year depreciation schedule for servers and network equipment. Burry’s analysis identified Oracle as having among the most aggressive depreciation assumptions relative to realistic hardware lifecycles, alongside Meta, Microsoft, Google and Amazon.

This is the core of Burry’s argument: the actual economic life of an Nvidia H100 GPU is closer to 2-3 years. Nvidia itself releases new chip generations annually now, and Jensen Huang has said publicly that when Blackwell starts shipping in volume, “you couldn’t give Hoppers away.” If a chip becomes competitively obsolete in 2-3 years but Oracle is spreading its cost over 6 years, the reported earnings look significantly better than the economic reality warrants.

The counter-argument, which is also legitimate, is that chips don’t have just one job. A GPU that’s no longer competitive for cutting-edge model training can be redeployed for inference, then batch processing, then analytics. CoreWeave’s CEO has pointed out that its A100 chips from 2020 are still fully booked, and its H100s from 2022 were immediately re-let at 95% of their original rental price when a contract expired. Amazon shortened its server depreciation life from 6 to 5 years in early 2025, explicitly citing the “increased pace of AI development” and took a $677 million hit to net income as a result. That’s what intellectual honesty about hardware lifecycles looks like. Oracle has not made an equivalent adjustment.

Why is this such a big deal, specifically for Oracle? Because Oracle is about to spend approximately $50 billion in a single fiscal year on hardware. At 6-year depreciation, the annual depreciation charge on that spend is roughly $8.3 billion. At 4 years, it would be $12.5 billion. That $4.2 billion difference flows directly into reported operating income. Oracle’s FY2026 non-GAAP earnings, already flattered by a $2.7 billion one-time gain from selling its Ampere stake, would look materially weaker under a shorter depreciation assumption. Watch whether Tuesday’s earnings call includes any updated guidance on depreciation policy. It likely won’t. But it should.

The NVIDIA relationship and the money loop

Oracle’s hardware dependency on Nvidia is worth understanding, because it sits at the centre of something that looks circular when you trace the money.

Oracle is reportedly spending around $40 billion on Nvidia GB200 GPUs to build out the Abilene, Texas Stargate data centre for OpenAI; approximately 400,000 chips in total. In August 2025, Oracle and Nvidia deepened their partnership further, with Oracle becoming one of the first hyperscalers to integrate Nvidia DGX Cloud Lepton and deploy GB200 NVL72 systems at scale. In October 2025, Oracle added a separate partnership with AMD, committing to deploy 50,000 AMD Instinct MI450 GPUs on OCI from Q3 2026, a hedge that gives Oracle supply chain optionality and positions OCI as genuinely chip-agnostic in a way its hyperscaler competitors, who are all building their own silicon, are not.

The circular dynamic is this: Nvidia announced a $100 billion partnership with OpenAI, with investment disbursed progressively as GPU-powered data centres are deployed. That capital largely recycles back to Nvidia through chip sales. OpenAI pays Oracle for cloud services under the $300 billion contract. Oracle uses that revenue, in part, to buy more Nvidia chips. The money flows in a triangle: Nvidia funds OpenAI, OpenAI pays Oracle, Oracle pays Nvidia. Each party locks in the others. It’s simultaneously a genuine strategic alliance and a structure where the interdependencies amplify the risks if any leg of the triangle weakens.

One important nuance: because Oracle is not building its own AI chips, unlike Microsoft, Google and Amazon which are all developing proprietary silicon, it has no reason to bias its infrastructure choices. It can buy whatever is fastest for each workload. The AMD partnership is evidence of this. That vendor neutrality is a genuine competitive differentiator for customers who don’t want to be locked into a single chip architecture. Whether it matters more than AWS or Azure’s deeper integration with their own silicon is a genuine open question.

The Bull Case

1. The backlog is not fiction.

$523 billion in RPO, growing at $68 billion per quarter, with acceleration in short-term conversion. That is a real contractual pipeline, signed by real companies. When the $25 billion bond sale attracted $129 billion in orders, credit investors were putting a stamp of approval on the quality of those contracts. They don’t oversubscribe five times on a backlog they don’t believe in.

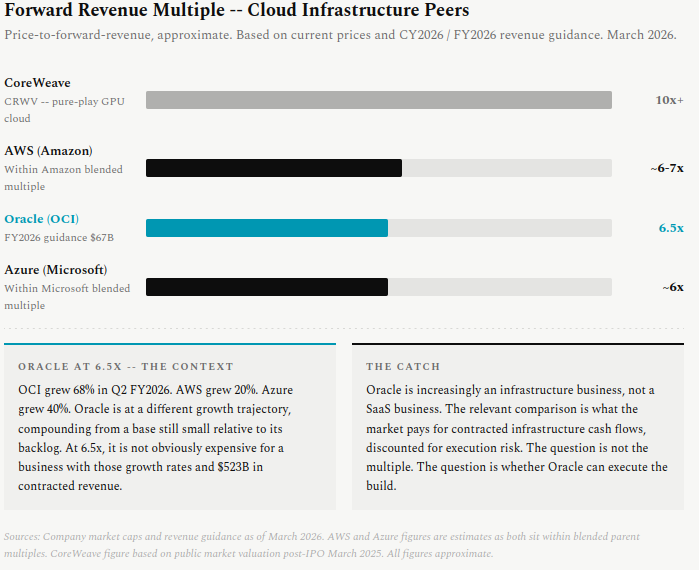

2. OCI is growing faster than any major cloud provider.

68% OCI growth and 177% GPU revenue growth are not numbers you see from a business losing. In Q3 2025, AWS grew 20% year-over-year and Azure grew 40%. OCI is at a different trajectory entirely, compounding from a base that’s still small relative to where it could be if the backlog converts as contracted.

3. The layoffs could be a genuine positive.

Cutting 20,000 to 30,000 people at a 162,000-person company is painful, but it’s coherent. Oracle has specifically flagged that some cuts target job categories it expects AI to replace. If the reported $8-10 billion in annual cash flow savings materializes, Oracle’s free cash flow picture changes significantly heading into FY2027. A company simultaneously burning capex and improving its operating cost structure is a very different story from one just burning cash.

4. The stock has priced in a lot of bad news.

56% off the 52-week highs on a company with $523 billion in contracted revenue and OCI growing at 68%. The pessimism is priced in. The question is whether it’s warranted.

5. The multi-cloud strategy is a second growth engine.

The 817% growth in multi-cloud database consumption might be the most underappreciated number in Oracle’s results. It means Oracle is generating revenue inside its competitors’ clouds. Customers paying Oracle whether they host on OCI, AWS or Azure. That scales without Oracle having to build a single new data centre.

The Bear Case

1. The balance sheet is genuinely stretched.

Total debt past $124 billion. Capex of approximately $50 billion expected in a single fiscal year. Free cash flow of negative $10 billion in one quarter. Oracle’s credit rating is BBB from S&P with a negative outlook. A downgrade would raise borrowing costs on an already enormous debt load. There’s not much margin for error if revenue conversion takes longer than planned.

2. The OpenAI concentration is a specific and serious risk.

S&P flagged that OpenAI could account for more than a third of Oracle’s revenues by FY2028. That is extraordinary customer concentration for a company of Oracle’s size. Oracle’s ability to collect depends on OpenAI remaining solvent and continuing to scale. If OpenAI’s competitive position weakens, or the relationship deteriorates, the revenue impact would be immediate and material.

3. Revenue has missed estimates in eight of the last ten quarters.

The bull case requires Oracle to accelerate revenue growth to 19%+ in Q3 and sustain from there. The track record on delivery is mixed. Converting the RPO backlog depends on building data centre capacity on time. That’s a construction and financing execution problem, not a software delivery problem, and it’s not something Oracle has a proven track record on at this scale. Data centre builds routinely face delays: permitting, power infrastructure, grid connections, equipment lead times, and contractor availability are all variables Oracle doesn’t fully control. A six-month delay in a gigawatt-scale facility doesn’t just push revenue; it pushes the entire RPO conversion schedule and extends the period of negative free cash flow. The Blue Owl situation demonstrates this isn’t hypothetical.

4. The financing dependency is a real constraint.

Blue Owl Capital pulling from a $10 billion data centre project was a warning. Banks have reportedly retreated from project financing for Oracle, doubling borrowing costs on some projects and stalling construction starts. If Oracle can’t fund the build, the capacity doesn’t come online, the contracts don’t convert, and the RPO figure becomes increasingly theoretical.

5. The co-CEO transition adds execution uncertainty.

Replacing a single experienced CEO with two new ones simultaneously, at the moment the company is executing the most complex and capital-intensive expansion in its history, is a risk. Magouyrk and Sicilia are deeply operational insiders. But co-CEO models often create ambiguity about accountability.

6. The securities class action is an overhang.

Securities fraud suits have been filed on behalf of investors who bought between June and December 2025. The allegation is that Oracle misled investors about its ability to rapidly convert capex into revenue. These cases are early stage, but they add legal cost and management distraction at a moment when execution is everything.

Valuation Snapshot

At approximately ~$153 per share, this is how Oracle looks today.

Oracle is increasingly an infrastructure business, not a SaaS business. The relevant valuation frame is what the market is willing to pay for contracted infrastructure cash flows, discounted for execution risk, not what multiple Salesforce trades at.

At $67 billion in FY2026 revenue guidance and a $440 billion market cap, you’re paying about 6.5x forward revenue. For context: AWS trades at roughly 6-7x forward revenue within Amazon’s blended multiple, and Azure is embedded in Microsoft at a similar range. CoreWeave, the pure-play OCI rival, has traded above 10x revenue since its IPO. On that basis, Oracle at 6.5x is not obviously expensive for a business growing 19%+ at the total level, with cloud at 34% and OCI at 68%, and $523 billion in contracted future revenue. The question is entirely about execution risk on the capex cycle and whether the cash flows from the completed infrastructure justify the capital deployed.

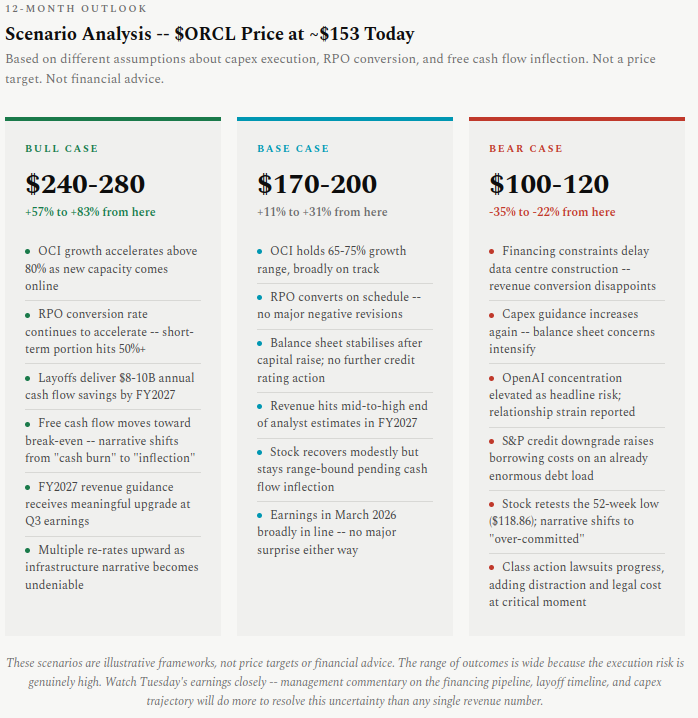

Scenario Analysis (12-Month View)

The following three scenarios model what Oracle’s stock could look like over the next twelve months, based on different assumptions about capex execution, RPO conversion speed, and whether the layoffs deliver the expected cash flow improvement.

Final Thesis

There are two ways to look at Oracle right now, and they lead to completely different conclusions.

The first view is that this is a 49-year-old enterprise software company that looked at the AI wave and made a bet so large it has distorted the balance sheet, stretched the credit rating and is now cutting tens of thousands of jobs to try to fund infrastructure it may not be able to build on schedule. The revenue misses, the capex overruns, the class action lawsuits, and the Blue Owl pullout are all pointing in the same direction. And at the moment the company needs its most experienced leadership, the CEO who ran the business for eleven years just departed.

The second view is that $523 billion of contracted revenue from the most important companies in AI, a cloud infrastructure business growing at 68%, and a $25 billion bond sale that attracted five times the demand are all telling you something different. The people who actually looked at Oracle’s contracts and network architecture and decided to deploy capital in size believed the story. And the 56% drawdown is the market’s short-term anxiety about spending that won’t fully convert until FY2028-2030, priced into a business whose forward revenue visibility is arguably the strongest of any enterprise tech company right now.

The risks are real. The OpenAI dependency is a genuine concentration risk. The balance sheet is genuinely stretched. Eight revenue misses in ten quarters is a real pattern. The absence of any insider buying during this drawdown is a signal worth sitting with.

To be direct: this piece leans bullish. Not because the risks aren’t real, but because the asymmetry at current prices is hard to ignore. At $153 with $523 billion in contracted backlog, OCI growing at 68%, and the largest insider owning 41% of the company and not selling a single share, I know which bet I’d rather be on if you forced me to choose.

Watch Tuesday closely. The numbers matter, but what management says about the layoffs, the financing pipeline, and whether capex guidance moves is what will drive the reaction. This is a setup where the next twelve months will look either obvious in hindsight or deeply painful, and there isn’t much in between.